⛰️ The Climb: July 2021

Welcome to The Climb!

“If you want to go far, go together” is a mantra we carry close to our hearts at Sherpa, as we know just how critical collaboration is to venture, especially in emerging ecosystems like Africa. The success of M-Pesa wouldn’t have been possible without central bank partners; similarly, Paystack’s ecosystem of financial services partners were also critical to their rapid success. In the last month, we’ve seen both Koa and Moneymie announce their own major partnerships to unlock critical institutional infrastructure and deliver stronger value to their customers. We couldn't be more excited for them!

At Sherpa Ventures, we’re rarely the only investors in a round, and it was awesome to announce our Payhippo investment with some of our friends who have global, local and deep sectoral expertise. We’re grateful to be able to co-invest and back founders in Africa together with some of the best in the business!

We also had a chance to get together with some of the most thoughtful leaders in African venture this month – like Lewam at Village Capital and Chris at Timon Capital – to pool our thoughts into a piece curated by Mario at The Generalist that spotlighted the African startup ecosystem to a global audience. 🌍

Finally, we couldn’t be prouder to be building Sherpa Ventures alongside future game-changers looking to break into venture. We’re so excited to welcome three of our very first Venture Associate Fellows (graduate degree not required!) who’ve been working alongside the team through all aspects of what we do!

Until next time! Stay healthy and stay collaborative!

- Aaron

PORTFOLIO HIGHLIGHTS ⭐️

Payhippo announced its fundraise! The Nigerian fintech leverages AI to provide seamless on-demand loans for SMEs in under three hours, regardless of their credit histories. Their $1 million pre-seed round drew interest from other prominent early-stage investors, including Ventures Platform, Future Africa, Launch Africa, DFS Lab, Hustle Fund and Mercy Corps Ventures, among others. With the new capital, Payhippo will focus on hiring for key roles and expanding to other Nigerian markets, as it looks to bridge the $158 billion SME financing gap.

Koa, a Kenyan fintech digitizing savings and investment, has partnered with leading African asset manager Britam. The partnership will enable Koa customers to gain easy access to low-risk investment opportunities through the Britam Money Market Fund. Read more about this big announcement and what this means for Kenyans here; alternatively, watch a quick clip from Kenyan Broadcasting Corporation from their press event.

The Central Bank of Nigeria (CBN) formally approved Moneymie’s relationship with Venture Garden Group as an investor and payout partner for Nigeria. This frees Moneymie from taking up any additional regulatory burden in Nigeria.

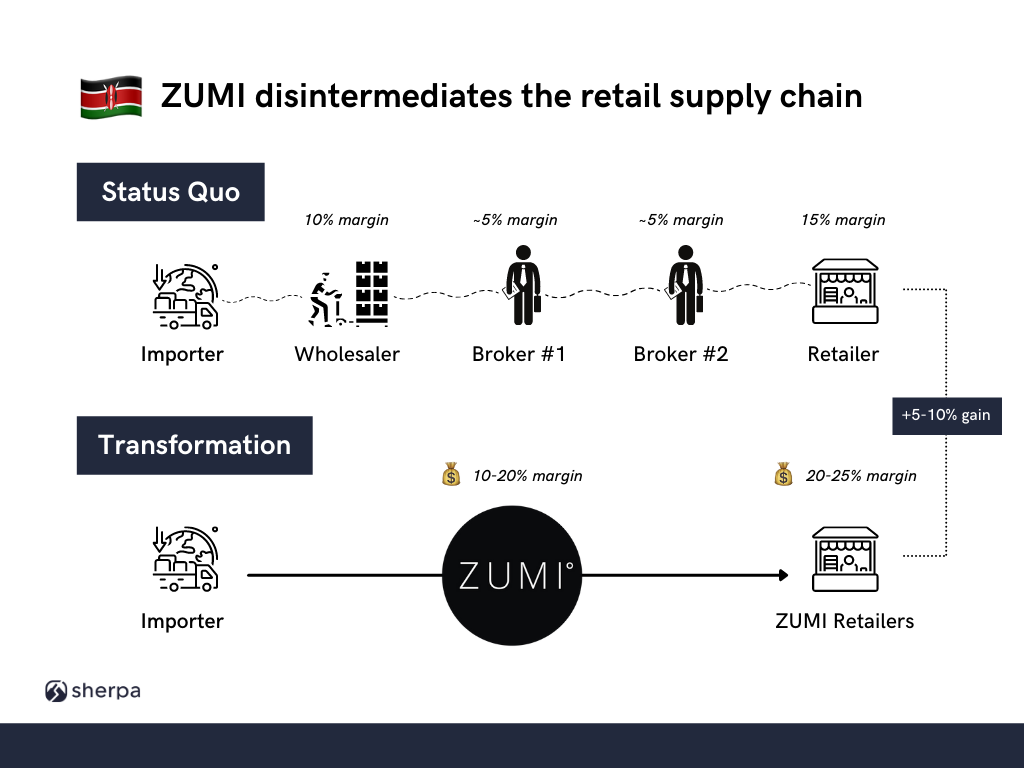

ZUMI secured a partnership with Pezesha, a digital lending platform for SMEs, to provide affordable working capital across the value chain for Africa’s network of clothing retailers.

WHAT’S NEW WITH SHERPA 🚀

Our team onboarded our first cohort of Venture Associate Fellows! Meet Jordan Wolken, Jessica Ajoku, and Arinze Obiezue.

Managing Partner Aaron Fu was featured as a contributor to the Tech in Africa brief by The Generalist that covered the key market opportunities and challenges of the African tech and venture capital ecosystem.

We published an article on our Medium publication profiling one of our portfolio companies, ZUMI, and discussing why we believe in their mission to connect African apparel wholesalers and retailers in a transparent, affordable marketplace.

WHAT WE’RE READING 📖

How Nigeria can solve its tech talent gap 👉 Link

A recent Ernst & Young report on the state of fintech in Nigeria unearthed the key dynamics underpinning the burgeoning industry. Despite Nigerian fintechs raising $439 million in 2020 — equivalent to 20% of the amount raised by all African tech startups — talent supply has not kept pace with hiring demand. In the EY report, attracting and retaining developer talent was cited as the top barrier to growth for fintechs, as skilled data analytics, cybersecurity and software engineering professionals, in particular, remain the most sought after yet more likely to seek remote or overseas opportunities. Nigeria’s rising inflation and consistent devaluation of the Naira against the U.S. dollar have caused top talent to seek foreign employment as a hedge against unpredictable currency risk. Time will tell whether this trend will continue.

Why this matters: Nigerian fintech is the most well-funded subsector of the African tech ecosystem; absent a strong local talent pipeline to fill key roles, companies may prolong hiring timelines, go months without vital employees, opt to hire part-time interns or pay more for overseas talent. If this trend gets worse, it could have major consequences for operators and investors who are active (or would like to become active) in the Nigerian fintech space. While well-funded startups like Paga and Flutterwave will have no problem attracting quality engineers, smaller and less mature fintechs already feel the talent gap to a relatively greater extent.

Though there is no easy solution, boosting the supply of local talent will require long-term thinking via collaboration between regional governments, startups and corporations. Doubling down on early STEM education, creating new upskilling programs for developers, crafting education legislation and forging university partnerships should all form part of a strategy to deepen local talent pools.

The Exits Are Coming: Africa’s Opening Act 👉 Link

In The Next Billion Substack, Juan Gabriel documents the trajectory of the African tech ecosystem. He argues that tech on the continent has evolved in three stages tolerating risk and market returns:

Official Aid – the original non-capitalist: Official Development Assistance (ODA) has existed in Africa since countries gained independence; for decades, this capital flow from the West was the main source of investment on the continent. Gabriel argues that ODA built some of the basic infrastructure that helped propel the African tech ecosystem to stage 2 (because ODAs were grants and the money was rarely expected back)

Impact investors – where no private actor would go: Impact investors have flooded the African market over the past 10-20 years, as the Millenium Development Goals (and now Sustainabile Development Goals) have set the framework for inventors to fund companies “that no private actors would fund, but which were beyond the purview or resources of ODA.” With a larger risk appetite, and motivations that extend beyond profit, impact investors have shown that smartly allocated capital can ‘do good’ – even if it achieves below market returns.

VC – from venture to frontier: Over the last five years, Gabriel argues that we have now advanced to the third stage of African tech. This stage is defined by venture firms actively courting market-validated returns in order to make their fund economics work. VCs investing in Africa now compete with impact investors for deals; this is neither good nor bad, Gabriel posits, but at least it is a sign of a maturing ecosystem.

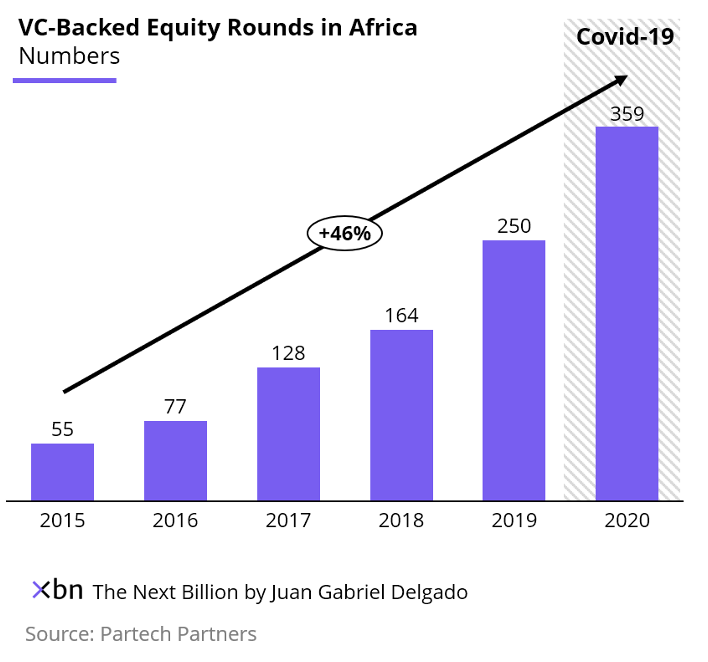

While Osarumen Osamuyi from The Subtext broke down the ecosystem’s growth in a different way (via experimentation, scaling and liquidity as three distinct phases), both Gabriel and Osamuyi believe that African tech is on the cusp of seeing some bigger exits for investors. After seeing Paystack, Send and other notable companies exit this year, one of Gabriel’s main takeaways is that “there are healthy multiples that validate product-market fit for VC-backed investments in Africa.” Coming on the heels of 2020 being the best year for M&A on the continent, we – like Gabriel – also tend to be bullish about the future of tech on the continent.

Lateral Thinking: Open Banking and Embedded Finance in Africa — Part 1 👉 Link

Open banking purports to change the relationship between banks, customers and their data by allowing customers to centrally manage all of their financial products through a single app. Arguably, it is the biggest trend in financial services since the advent of the ATM. OnePipe, Mono, Okra and other fintechs are all pioneers in the open banking space, leveraging APIs to digitally connect bank accounts to financial applications.

Our friends at Lateral Capital have released two parts of a three-part series on how the open banking movement originated globally, how incumbent banks are responding, and why embedded finance is sweeping across the continent. Though dense, this piece is rich with context that provides helpful insight for those looking to learn more about this emerging opportunity on the continent.

Corporate Venture Capital is widely misunderstood but makes sense for Africa 👉 Link

Despite Corporate Venture Capital (CVC) becoming an established corporate development activity on par with R&D and M&A spending globally, CVC has a pretty limited track record in Africa. Peter Kisadha, Research Associate for Future Africa, explains why CVC hasn’t gained as much steam on the continent as it has in other parts of the world. Surprisingly, except for Jumia and Takealot, which raised from MTN Group and Naspers respectively, no African startup that’s raised more than $100 million counts a top African corporate among their backers. Interestingly, with African banks being the largest corporates on the continent (and the most profitable relative to global peers), one would expect them to be much more active in making startup investments to access potentially lucrative partnerships and innovative technology. That said, they have not made much of a foray into CVC. As Kisadha notes,

“Historically, African corporates have been cagey and defensive in their relationship with startups particularly because of the fear that allowing startups free rein might hurt their business. As a result, they have often stacked odds against new entrants or tried to compete by launching copycat solutions. A case in point is the ongoing dispute in Senegal between Wave and Orange.”

However, as Kisadha points out, there is usually much more to gain for startups, VCs and corporates to work together than continue along the same pathway. CVC investments can help startups overcome structural barriers, set up new distribution channels, grow brand credibility and leverage existing customer segments. For VCs, CVCs can help bring in new capital and expand networks. And corporates themselves can deploy CVC arms to outcompete their competitors by gaining access to proprietary technology and market-validated financial returns. If set up properly, startup-corporate-VC partnerships can be hugely beneficial for each stakeholder; going forward, expect to see more CVC arms popping up in Nigeria and elsewhere on the continent, as thus far most corporate activity in this space has been concentrated in South Africa.

The inside story of how an ambitious African cryptocurrency startup failed 👉 Link

Honest accounts of startup failure are hard to come by, so it’s a big deal when we become privy to one. This feature about an ambitious cryptocurrency startup, and how the company fell out of place after raising $600,000, comes with some important, universal tips for up-and-coming founders. We’re sharing our favorite takeaways here:

Don’t build a tech startup without technical know-how: teams with technical co-founders and/or someone who’s worked in the industry beforehand will be able to spot gaps in the market more easily

Don’t outsource tech development: it will cost you more and make it harder to scale later. Instead, focus on networking well and crafting a really compelling sales pitch to attract local, in-house talent

Seek out guidance from experienced mentors: enlisting accomplished individuals with industry knowledge to serve as advisors will pay dividends for founders in the long-run. Others have attempted to solve similar problems before, and it behooves founders to learn from prior experiences to avoid repeat mistakes

Be lean-minded: reduce costs while building an MVP, and test iterations of your product with sample customers in the market as quickly and often as possible early-on. Do this on a low budget.

Conduct lots of customer surveys and research before raising funds or launching anything: don’t rush the product into the marketplace before proving that there is sufficient demand for it to begin with

Make sure to have internal alignment on company priorities among co-founders: clearly define roles and responsibilities and articulate a company ‘North Star’ everyone can rally around. Doing so will make it easier to stay united when hurdles arise

Stop saying you want to bank the unbanked 👉 Link

As investors who believe in technology-driven businesses, we are sometimes guilty of viewing tech as a singular panacea for all existing problems in Africa. While fintech has attracted the lion’s share of startup funding on the continent — some of it going to companies claiming to “bank the unbanked” (or something similar) using blockchain technology — there is room for caution when assessing one company’s ability to address such a fundamental problem. As Yaya Fanusie, Adjunct Senior Fellow at the Center for a New American Security, writes for Forbes:

“The main assumption to check around banking the unbanked is around the cause of peoples’ unbanked status. It is assumed that those who lack financial services primarily need a better way to access them. Technology is perceived as an ideal solution.”

Yet Fanusie goes on to cite numerous development studies which show that the two main underlying factors influencing why people remain unbanked are 1) a lack of money, and b) a dependence on family members who already have an account (cultural and familial ties matter!). In sum:

“People mainly lack financial services because they lack income and not the other way around. So, to effectively bank the unbanked, the key problem to solve is how to help people generate more income. This prime factor is ignored by many technologists because when it comes to helping people gain wealth, there is no singular app for that.”

Founders building fintech solutions targeting the unbanked, then, should consider ways to integrate previously unmarketed groups into the financial system by helping them build wealth. Blockchain startups may have a role to play in this endeavor, Fanusie writes, but the jury is still out. In the meantime, a shift in mindset needs to happen:

“It also is a time to check the assumptions guiding our endeavors. For those who want to assist people in poverty, we should not overemphasize their status as banking customers. Instead, we should help them gain success in markets that will allow them to generate more income and become financially empowered to access better financial services. Our aim should be to bring the unmarketed to the marketplace.”

We hope this is a reminder for founders to build products that address true customer pain points, rather than blindly applying technology to a problem without local context. Over time, we’ve found that the most successful African entrepreneurs are those with deep understanding of technology and local market contours. In fragmented marketplaces, fintech entrepreneurs who can expand their customer base by enabling customers to become banked through new income generation will find the most success.

OPEN ROLES IN SHERPA’S PORTFOLIO 🤓

Head of Finance @ Payhippo

Head Engineer @ ZUMI

Product Designer @ Money254